The Situation

The scenario models a 45-year-old running a profitable limited company. Salary is set at £12,570 (NI threshold) with £95,000 in dividends. The company contributes £40,000 a year into a SIPP — deductible for Corporation Tax. The household also holds a £950,000 main home and a BTL flat in an SPV.

The year-end question: should the employer pension contribution increase further, should more go into EIS/VCT for the 30% income tax relief, or should cash stay in the company?

Scenario dashboard — projection hero with KPI cards

What Wealth365 Showed

Wealth365 projects three scenarios side-by-side: (A) current mix, (B) employer pension up to £60,000 annual allowance, (C) £60,000 pension plus £20,000 EIS. Scenario C cuts personal income tax by £8,800 in year one, while adding £20,000 to the EIS portfolio at a net cost of £14,000.

The company-level wrapper analysis also shows the Corporation Tax saving from the higher employer pension contribution — a £7,600 CT saving at 19%.

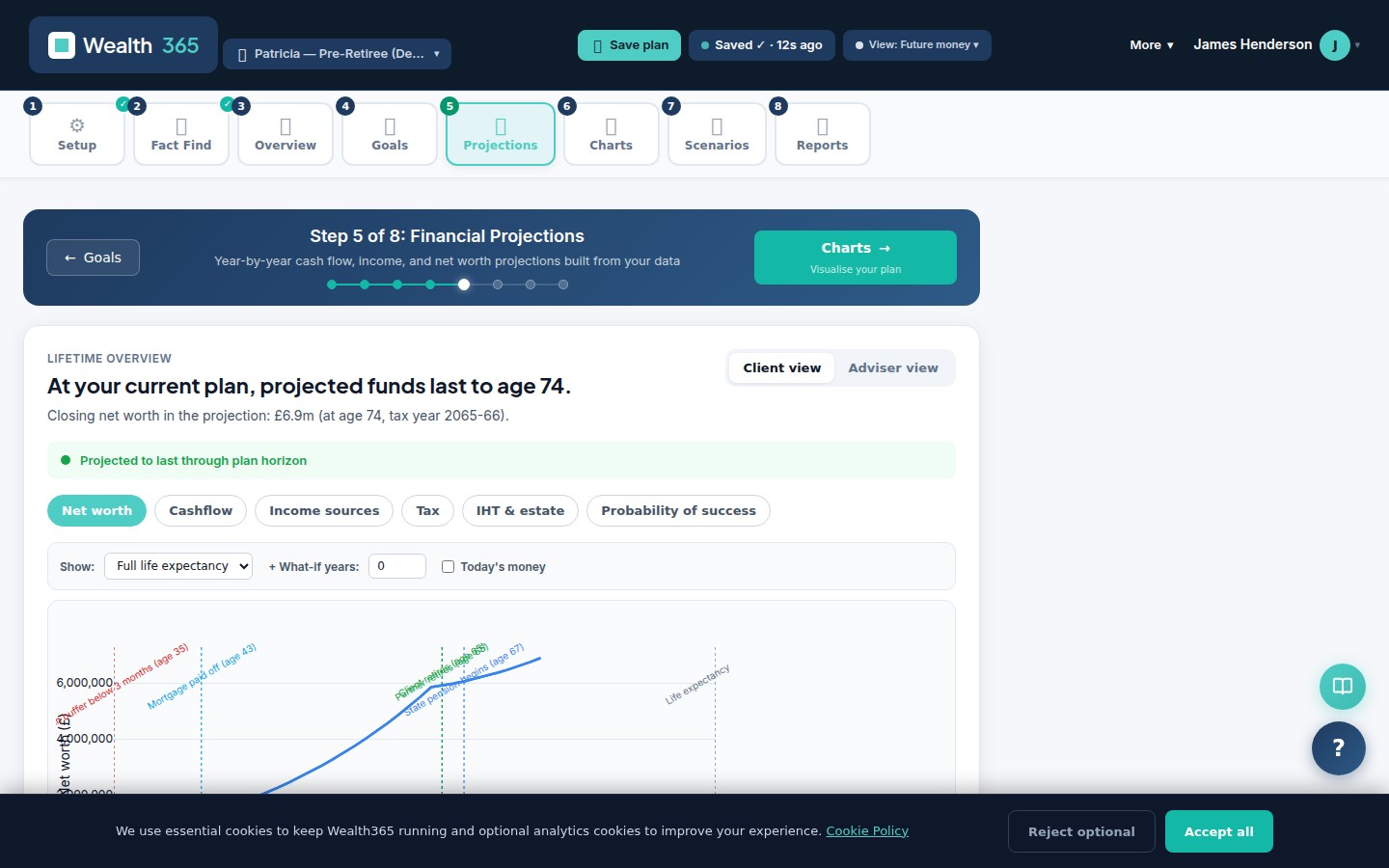

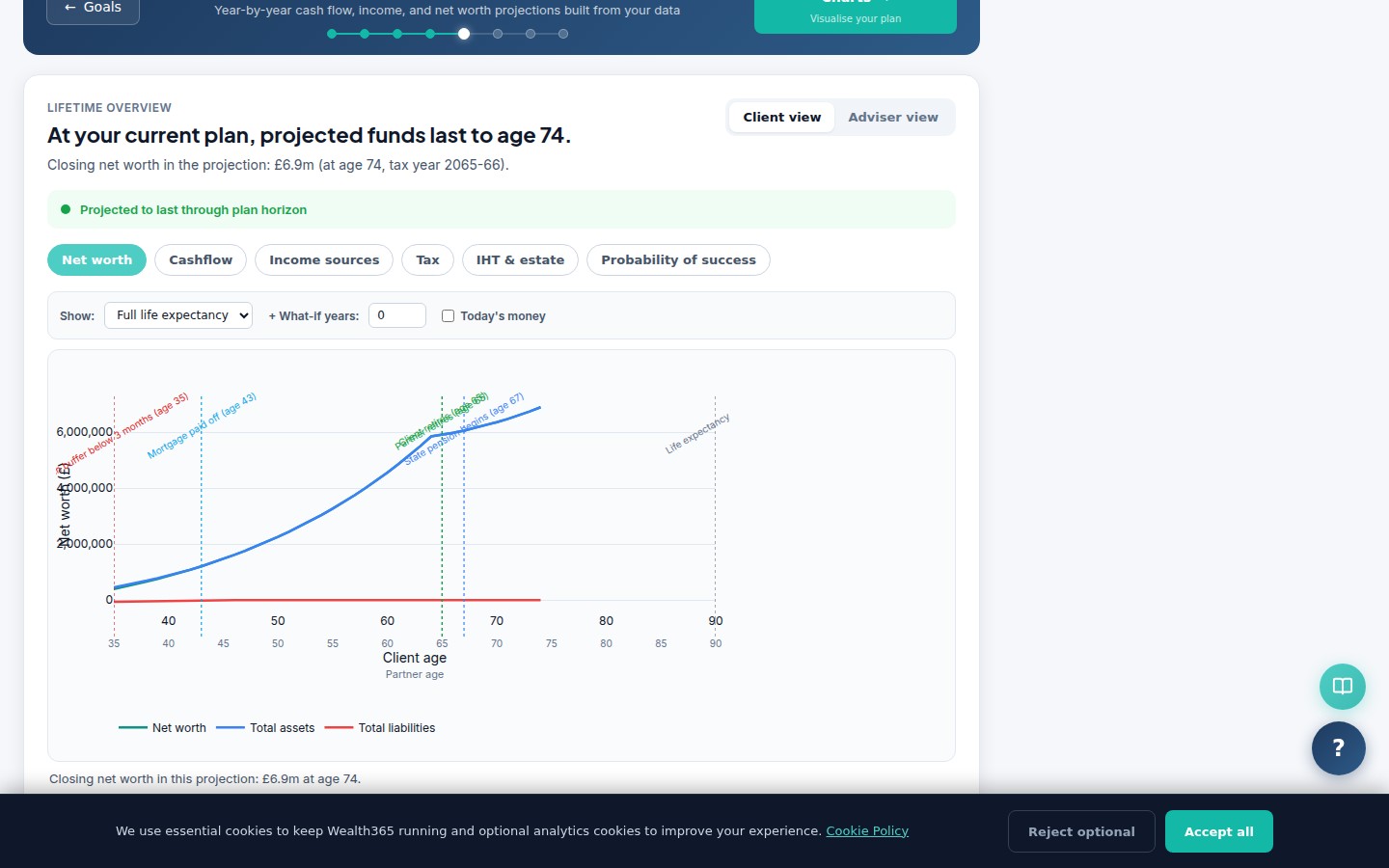

Year-by-year projection with income, expenses and net worth

The Feature That Changed Things

The wrapper optimisation tool in Fact Find → Surplus models each wrapper's effective tax rate against the director's marginal income position. At £95,000 dividends, employer pension has a 0% effective rate because the CT relief offsets the personal benefit.

The BTL SPV section correctly applies Section 24 mortgage interest relief at basic rate only, showing the true after-tax rental yield.

Wrapper mix analysis — salary, dividends, pension and EIS effective rates

KPI summary — on-track %, projected wealth at retirement, and sustainable income

Key Numbers from the Plan

Computed live from the Wealth365 projection ledger for this scenario’s seeded plan.

What They Did Next

Scenario C is adopted for the current tax year. The plan is re-run each January to set the year-end dividend level. The Multi-Year Financial Statements (Excel) export gives the accountant a full P&L, Balance Sheet and Cash Flow per year — the audit-ready evidence behind every extraction call.

Custom-branded PDF report — ready to share or save (Multi-Year Financial Statements Excel workbook produced from the same plan)