“Should I overpay my mortgage or invest the money instead?” is one of the most common financial questions for homeowners in their 30s. There is no single right answer — it depends on your mortgage rate, your expected investment returns, your tax position, and how much uncertainty you can tolerate. Here is how to think through it clearly.

Key takeaways

- Compare your mortgage rate to your expected after-tax investment return — above roughly 4.5–5%, overpaying starts to look competitive

- Overpaying delivers a guaranteed, tax-free return equal to your mortgage rate — investments deliver a higher but uncertain return

- Always fund employer pension matching before choosing between mortgage overpayment and investing — matched contributions are an immediate 50–100% return

- Check your mortgage for early repayment charges (ERCs) — most fixed deals cap overpayments at 10% of the balance per year

- Building your LTV down to the next tier (e.g. 75%) at remortgage time can reduce your rate meaningfully, adding a bonus return to any overpayment

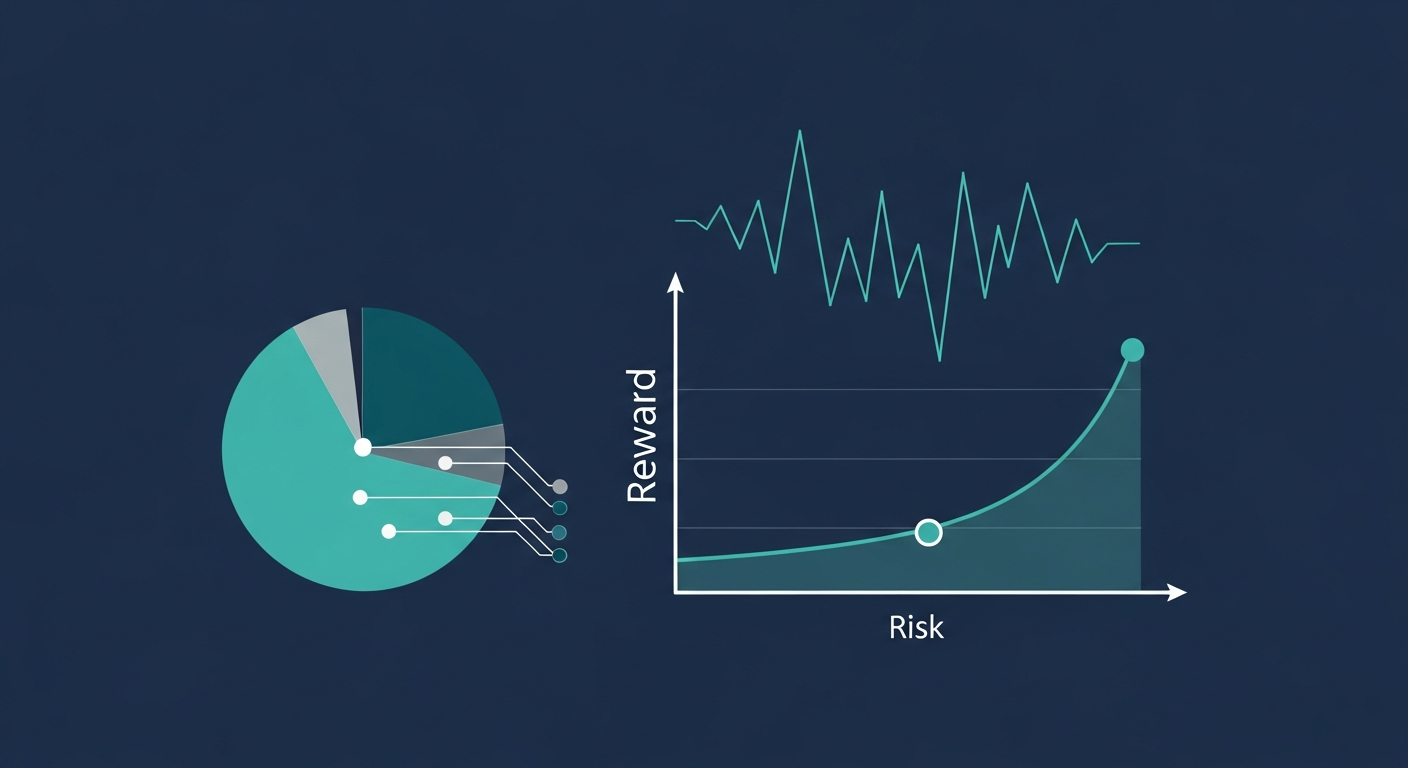

The Core Maths: Mortgage Rate vs Expected Return

At its most basic, the decision is a comparison of two rates:

- Your mortgage rate — the guaranteed, risk-free return you get from overpaying (you save the interest you would have paid).

- Your expected investment return — the potential (but uncertain) return from investing in stocks and shares, typically quoted as 5–8% per year in real terms for a globally diversified equity portfolio over the long run.

If your mortgage rate is 4.5% and your expected investment return after tax is 6%, the maths favours investing — you’re expected to make more by investing than you save in mortgage interest. If your mortgage rate is 5.5% and you can only access a 4% expected return after fees and tax, overpaying wins.

The complication is that the mortgage rate is certain and the investment return is not. A guaranteed 4.5% saving is not the same risk as a 6% expected return that might deliver 2% or 10% in any given year.

The Certainty Premium — Why Overpaying Has Hidden Value

There are three underappreciated reasons why mortgage overpayment is often more valuable than the headline rate comparison suggests:

- Guaranteed return. Overpaying your mortgage delivers a guaranteed, tax-free return equivalent to your mortgage rate. There is no equivalent investment with the same certainty. For risk-averse homeowners, or those with a high mortgage rate, this certainty has real value.

- Improves loan-to-value (LTV) faster. Overpayments reduce your mortgage balance, which means when you remortgage you may qualify for a lower LTV band with a better interest rate. In a rising or volatile rate environment, getting to the next LTV threshold early (e.g. 75% or 60%) can deliver a meaningful rate saving that compounds over the remaining mortgage term.

- Reduces financial stress. Carrying a smaller mortgage is measurably less stressful for many people. This is not irrational. Financial security has real value, and a paid-down mortgage creates options — the ability to take career risks, handle emergencies, or reduce hours without the same income pressure.

When Overpaying Your Mortgage Wins

Mortgage overpayment is likely the better choice if:

- Your mortgage rate is above 4.5–5% — At these levels, the guaranteed return from overpaying starts to look attractive versus the risk-adjusted return of equities, especially after investment costs and tax.

- You have already filled your pension and ISA allowances — These tax-efficient wrappers should generally be funded first (see below). Once they’re full, overpaying the mortgage is a sensible next step for spare cash.

- You are within 5–10 years of wanting to pay off the mortgage — Overpayments in the later years of a mortgage have proportionally more impact on total interest paid.

- Your LTV is close to the next tier — If you’re at 81% LTV and the next rate tier is at 80%, a targeted overpayment to cross that threshold can be highly efficient.

Use our projection tools to model exactly how much interest you would save at different overpayment levels, and compare the outcome against a projected investment return.

When Investing Beats Overpaying

Investing extra money is likely the better choice if:

- Your mortgage rate is low (below 3.5%) — At low fixed rates, the historical long-run return from a diversified equity portfolio has comfortably exceeded the mortgage rate, even after fees and CGT.

- You have unused pension annual allowance — Pension contributions attract 20–45% tax relief (and employer matching in a salary sacrifice scheme). This upfront relief makes pension contributions almost always a better use of money than mortgage overpayment, even at higher mortgage rates.

- Your mortgage has significant early repayment charges (ERCs) — Many fixed-rate mortgages limit overpayments to 10% of the balance per year without ERC penalties. If you’re already using your annual overpayment allowance, further “overpayments” would incur charges that wipe out the benefit.

- You have a long time horizon — If you’re 30 years from retirement with a sub-4% mortgage rate, the compound effect of 30 years of equity returns is hard to match.

Our financial planning tools let you model both paths side by side: input your mortgage details and your investment assumptions and see the projected difference in net worth at any horizon you choose.

The Practical Framework: Three Priorities Before You Choose

Before the mortgage vs invest question even applies, three things take priority:

- Emergency fund first. If you don’t have 3–6 months of essential expenses in easy-access savings, build this before overpaying or investing.

- Employer pension matching. If your employer will match pension contributions beyond the minimum (and many do), match it. This is an immediate 50–100% return on your money — there is no overpayment or investment that competes.

- High-cost debt. Credit card debt at 20%+ APR or personal loans at 8–12% should always be cleared before either overpaying a mortgage or investing. The return from eliminating 20% APR debt is guaranteed and untaxed.

Once those three bases are covered, the mortgage vs invest question is genuinely a close call for many homeowners, and the right answer often involves doing both in some proportion. A regulated financial adviser can analyse your complete picture — mortgage rate, tax position, retirement savings gap, and risk tolerance — and recommend the right split for you.

Important: This article is for general educational purposes only and does not constitute financial advice. Tax rules can change and individual circumstances vary. If you need advice tailored to your situation, please consult a qualified, FCA-regulated financial adviser. You can browse advisers in our adviser directory.