All investing involves some degree of risk. Understanding the different types of risk, and how spreading your investments can help manage it, is fundamental to making informed decisions about your savings and investments.

Key takeaways

- Risk is not just about losing money — inflation risk can erode your purchasing power too

- Higher potential returns generally come with higher risk

- Diversification spreads risk across different investments, reducing the impact of any single one performing badly

- Your time horizon is a key factor in determining appropriate risk levels

- Understanding your personal capacity for loss and emotional comfort with volatility helps guide investment decisions

What Is Investment Risk?

Investment risk is the possibility that your investments could fall in value or that the returns could be lower than expected. But risk is not just about losing money:

- Market risk — The value of investments can go up and down due to economic conditions, political events, or market sentiment.

- Inflation risk — If your returns are lower than inflation, your money loses purchasing power over time, even if the nominal value increases.

- Concentration risk — Putting all your money into one investment, sector, or geography increases your exposure if that area performs poorly.

- Currency risk — For international investments, changes in exchange rates can affect returns.

- Liquidity risk — Some investments (property, certain funds) may be difficult to sell quickly at a fair price.

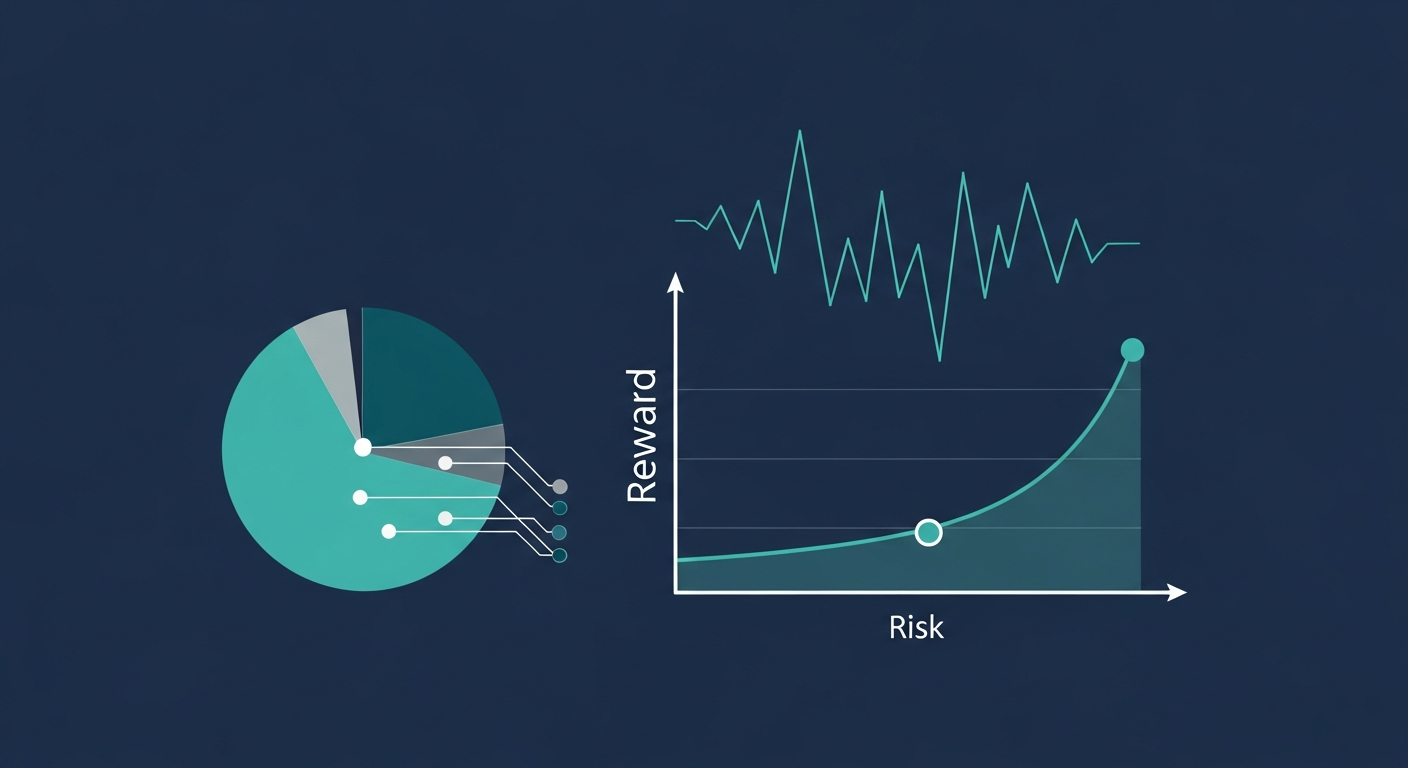

Risk and Return

Generally, investments with higher potential returns carry higher risk. Cash savings are low risk but tend to offer lower returns, especially after inflation. Equities (shares) have historically provided higher long-term returns but with more short-term volatility.

Common asset classes ranked roughly by risk (lower to higher):

- Cash and money market funds — Low risk, low return, protected up to £85,000 by FSCS

- Government bonds (gilts) — Relatively low risk, modest returns

- Corporate bonds — Moderate risk, better returns than gilts

- Property — Moderate to higher risk, potential for income and capital growth

- Equities (shares) — Higher risk, higher long-term return potential

- Alternative investments — (commodities, private equity, cryptocurrency) — Higher risk and complexity

Diversification: Not Putting All Eggs in One Basket

Diversification means spreading your investments across different asset classes, sectors, and geographies. The idea is that when one type of investment performs poorly, others may hold up or perform well, smoothing out your overall returns.

A diversified portfolio might include:

- A mix of UK and international equities

- Some bonds or fixed-income investments

- Property (directly or through funds)

- Cash or near-cash holdings for stability and liquidity

Multi-asset funds and target-date funds provide built-in diversification, which can be a straightforward option for people who prefer not to select individual investments. Our financial planning tools let you model how different asset allocations affect your long-term projections.

Time Horizon and Risk

Your time horizon — how long until you need the money — is one of the most important factors in determining how much risk is appropriate:

- Short term (under 5 years) — Lower-risk investments like cash or short-term bonds may be more suitable, as there is less time to recover from market falls.

- Medium term (5-10 years) — A balanced mix of assets may be appropriate.

- Long term (10+ years) — Historically, equities have outperformed other asset classes over long periods, despite short-term volatility.

As you approach a goal (such as retirement), it is common to gradually reduce risk — a process sometimes called "lifestyling" or "glide path" investing.

Understanding Your Risk Tolerance

Risk tolerance is personal and depends on several factors:

- Capacity for loss — Can you afford to lose some or all of this money without it affecting your standard of living?

- Time horizon — Longer time frames generally mean you can tolerate more short-term volatility.

- Emotional comfort — How would you feel if your investments fell 20% in a year? If that would cause you significant stress or lead you to sell, a lower-risk approach might be more suitable. A regulated financial adviser can help you identify the right risk profile for your goals.

- Other resources — Do you have other savings, property, or guaranteed income (like a DB pension) that provide a safety net?

Important: This guide is for general educational purposes only and does not constitute financial advice. Tax rules can change and individual circumstances vary. If you need advice tailored to your situation, please consult a qualified, FCA-regulated financial adviser. You can browse advisers in our adviser directory.